If you are one of the millions of regular Brits trying to improve their credit score, you are in good company. A lack of financial literacy combined with a carefree attitude towards managing my money as a university student left my credit rating in poor shape. Even after I secured my first job after graduating I still couldn’t shake free the shackles of my rather reckless past.

Close to a decade, later I am now in the process of building up my credit and improving my score steadily. The goal is to get to a point where I am eligible for financing my first home and finally get onto the slippery property ladder. An old County Court Judgement (CCJ) for a parking offence I wasn’t aware of committing has finally fallen off, which gave my score a 50 point boost. Only a couple of aged defaults remain and I am tantalisingly close to my target score of 400.

So why have I written this post and why should you read it? Well, if you are like me you want a good deal right? I have always been savvy when it comes to switching energy suppliers, hunting for the best car insurance quote or saving as much money I possibly can with cashback sites.

One thing I had not realised about switching suppliers though until I started monitoring my credit file religiously, is that it can put a dent in your credit score. I will explain why next.

Hard Search vs Soft Search

Relax, this has nothing to do with random stop and search activity on the streets of London.

A search or credit check is when a potential lender looks at your credit file so that they can have a better understanding of your borrowing history.

Borrowers carry out different types of searches depending on the nature of your application. The two types of searches are:

- Soft search

- Hard search

Let’s look a little bit more into the two different types of credit searches.

Soft Credit Search

Lenders will sometimes refer to a soft search as a quotation search. In this instance, a potential lender looks at your credit information but does not access your entire credit report.

A soft search is a preliminary credit file check and is invisible to other creditors. Only you will have access to any soft searches on your file. The good thing is that soft searches do not affect your credit score.

Examples of soft searches include the following:

- Identity checks by lenders

- When you access your own report through Clear Score, Experian or other credit checking agencies

- Financial product eligibility checks (these are becoming quite popular as more lenders want to promote their products)

Now, let’s move on to the more exciting stuff.

Hard Credit File Search

Sometimes known as credit application checks or hard checks, a hard search happens when a potential lender (credit car company, insurance financing company, energy provider etc) accesses your credit report to assess creditworthiness.

A hard searches leave marks on your credit file, like footprints in the sand on the beach. These marks are visible to other potential lenders(and whether your application was approved or declined).

Hard searches typically stay on your report for 12 months, although debt collections can last for about 2 years.

When do prospective lenders perform hard searches?

Below are some of the situations under which potential creditors will perform a hard search on your credit history so they can that little bit deeper:

- When you apply for a credit card, mortgage, loan or take out car finance

- When you switch energy supplier or car insurance provider

- When you change to a different mobile phone contract

If you are unsure whether a utility company will perform a soft search or a hard search, ask before you switch. I had to find out the hard way as I didn’t realise this would have such an impact on my score.

More often than not, a hard search will impact your credit score. The silver lining is that, if you keep your borrowing under control, the impact is short term.

However, a quick succession of hard searches appearing on your credit record may send the wrong signals. Creditors view this as a sign of desperation like you are struggling financially and can’t manage your existing debt. Therefore, if you are considering some financial spring-cleaning such as switching insurers, utility providers, bank accounts etc, you may want to space this out over the year.

Also, if you are more interested in building your score in preparation for a mortgage application, it may suit you better if you give yourself a ban from making changes to any existing credit arrangements.

How Much Will A Hard Search Damage Your Score?

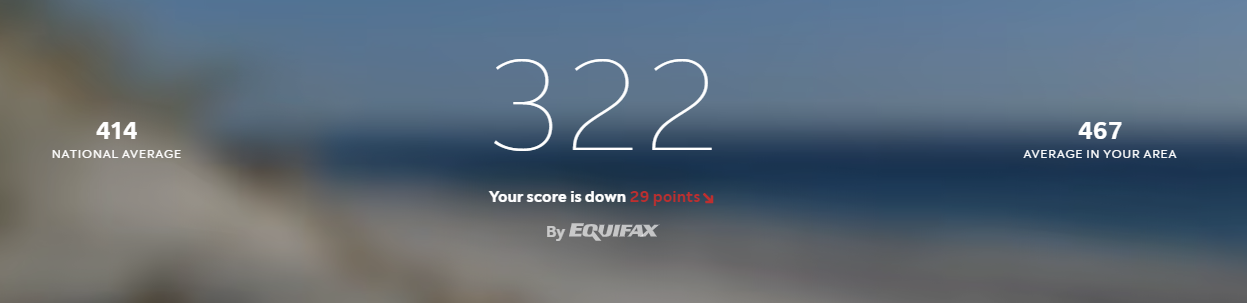

In my case, following a hard credit search by a prospective utility provider, my score dropped 22 points. I am not sure if this would be a standard impact or it depends on your personal circumstances. However, if you are trying to keep your score as high as possible for a mortgage application, this may throw some spanners in the works.

I went ahead and switched to the new supplier and I thought that would be the end of it. However, because I opted to pay my bill via direct debit (essentially consuming the energy on credit), my score suffered another hit. Let me explain why.

So when the utility provider accessed my credit file and registered as a hard search, they cost me 22 points. When I signed the contract, a new credit account was added to my credit file, and this cost me a further 29 points. All in all, the process of switching utility providers impacted my credit score by 51 points.

Now, just imagine if you had decided to save some money by reviewing all your current credit commitments (car insurance, utilities, broadband, mobile phone provider, life, pet and contents insurance). I’m not saying all these would have had an impact on your score, but from my experience, there is a big chance they would have and your score would have been down considerably.

So, what can you do to minimise the short-term damage switching financial products can have on your credit score? Let’s talk about that in the next section.

Reduce The Impact Of Hard Searches On Credit Score

As you can see, something as simple as being money-savvy and looking for a better utilities deal can put a dent in your credit score. The good thing is that this is commonly a temporary blip on the road to a better score (unfortunately at the time of writing my credit score is yet to recover the 51 point hit ouch!). So, what can you do to minimise the damage switching suppliers can have on your credit rating? Here are a few ideas:

- Always check with potential suppliers if they will perform a soft or hard search

- If you are going to do some financial spring cleaning and switch insurance, utilities and banks etc, spread them out over the year. Remember more than 3 hard searches on your file within a year becomes a red flag for potential creditors.

- Finally, if you are building your credit up for a new mortgage, remortgage or a loan, it may well serve you better to defer switching utility providers until your application for credit has gone ahead.

Reducing the impact of hard searches is a critical aspect of repairing your credit score. You may pay a little more for your gas and electricity now, but staying with your current supplier instead of switching may prove a better deal in the long run.

Final Words…

Gas and electricity costs are going to go up in 2022, there is no doubt about that. Many suppliers failed to plan for the rampant increases in the wholesale price of natural gas in 2021 and they will seek to recover costs in the new year.

If you are considering switching suppliers, make sure you are prepared to take the hit that’s surely coming when the new provider performs a credit check. Looking to boost your credit score, sticking with your current supplier may be the best way to go.

Found this article is useful and you have a friend who can benefit from it, please feel free to share it with them.